Subscribe to our newsletter

Stay informed about our latest developments and updates!

Why LTV management separates survivors from casualties

The past four months reminded Bitcoin borrowers of a timeless truth: leverage that feels comfortable in rising markets becomes dangerous when prices turn.

What happened

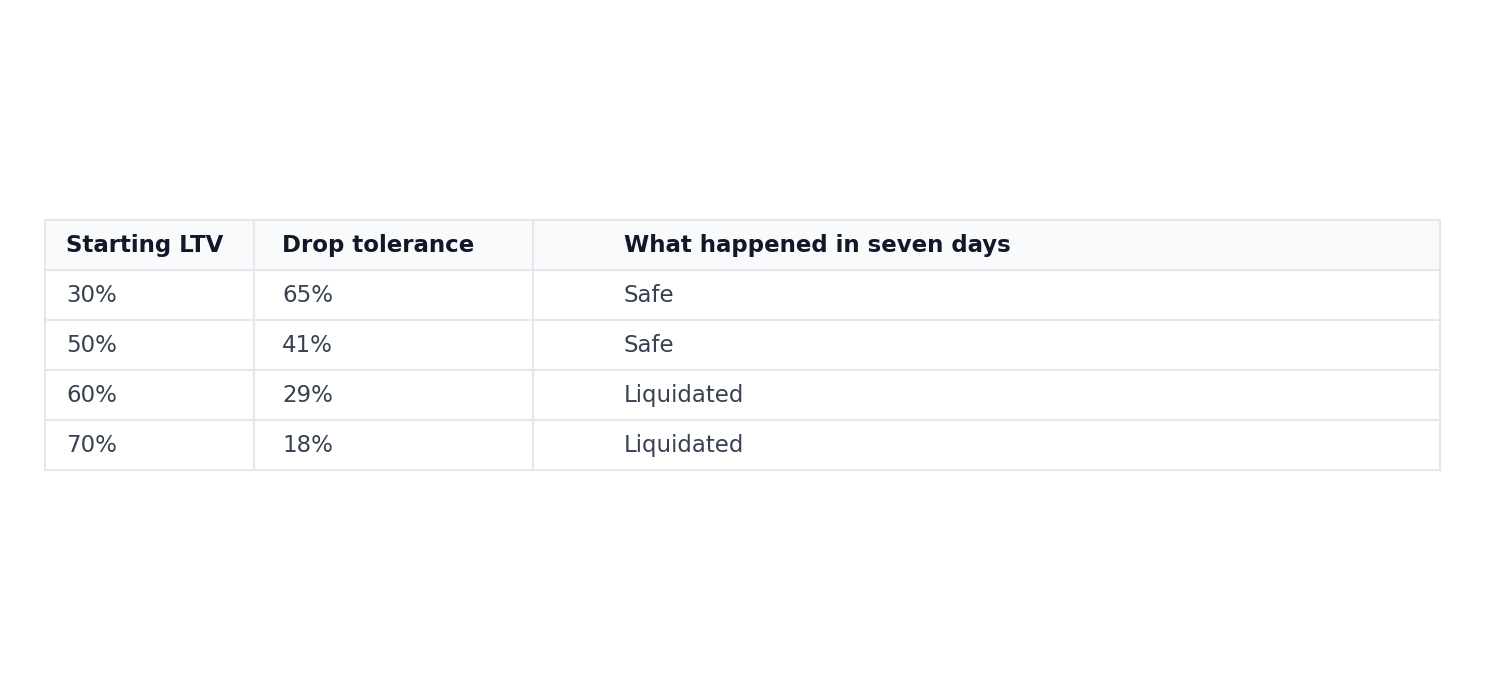

On October 6, 2025, Bitcoin reached its all-time high of $126,000. Four months later, on February 5, 2026, it touched $63,000, a decline of 52% from peak to trough.

The move was not gradual. After months of slow decline, the final leg came fast: Bitcoin dropped 33% in a single week, falling from $90,000 to $63,000. More than $2 billion in leveraged positions were liquidated across the market. Borrowers who had entered loans at 50%, 60%, or 70% LTV watched their collateral sold at market bottom, crystallizing losses that proper planning could have avoided.

This pattern is not new. It has appeared in every major market correction across modern financial history.

The difference between preserving wealth and losing it lies entirely in preparation.

The mathematics of safety

The relationship between starting LTV and survival is not subjective. It is mathematics.

From all-time high to bottom: 52% decline ($126,000 to $63,000)

Anyone who entered a Bitcoin-backed loan at 50% LTV or higher since October and did not manage their LTV actively was liquidated. Collateral accumulated over months or years was sold automatically at the worst possible price.

In one week alone: 33% decline ($90,000 to $63,000)

Borrowers at 60% LTV had just 29% buffer. A 33% drop in seven days erased it entirely, leaving only a few days to add collateral or face forced liquidation at the bottom.

Your LTV management plan: before you need it

The time to prepare for a correction is not during the correction. It is now.

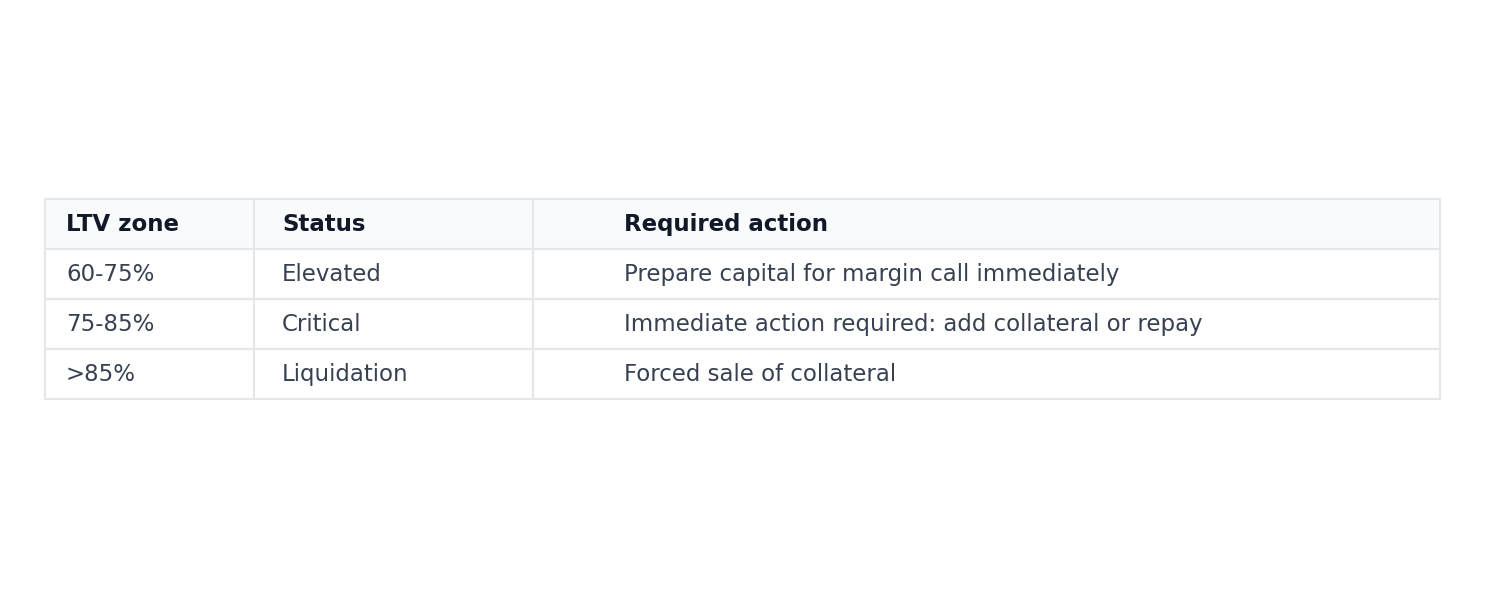

Know your thresholds:

Have capital ready. When Bitcoin dropped 30% last week, borrowers with reserves could add collateral and restore healthy LTV ratios. Those without reserves became forced sellers, joining the $2 billion in liquidations.

Calculate your response in advance. If your LTV reaches 75%, how much collateral must you add? How much must you repay? Know these numbers before the margin call arrives.

The lesson from February 2026

The borrowers who were liquidated made their decision months earlier, when they accepted high LTV ratios without a management plan. The borrowers who survived made their decision months earlier too, when they chose conservative LTV and prepared reserves for exactly this scenario.

A 30% LTV borrower in October still holds their Bitcoin today. A 50% LTV borrower lost nearly everything at the bottom. The difference was not luck. It was mathematics.

If you hold a Bitcoin-backed loan, review your LTV today. If you are considering one, start at 30% maximum ,not because it feels necessary now, but because it will prove essential when the next correction arrives.

This analysis draws from The Bitcoin Lending Standards 2026, an article about Bitcoin-backed lending: covering loan mechanics, historical precedent, risk management protocols, and institutional best practices.

Bitcoin-backed loans are provided by Blockrise Lending B.V. A group company of Blockrise Capital B.V. Bitcoin-backed loans are not regulated under MiCAR.

Download the PDF to read the full article.