Subscribe to our newsletter

Stay informed about our latest developments and updates!

Mapping the point of no return in Bitcoin lending

Bitcoin-backed lending has grown into a multibillion-dollar market, yet the question of how much collateral a lender needs across Bitcoin market cycles has never been empirically tested with a decade of daily data.

The Loan-to-Value ratio (LTV) represents the loan amount as a percentage of the Bitcoin collateral posted.

This paper stress-tests daily loan originations from January 2016 to March 2026 across four LTV tiers, measuring the worst-case outcome over each loan's full term.

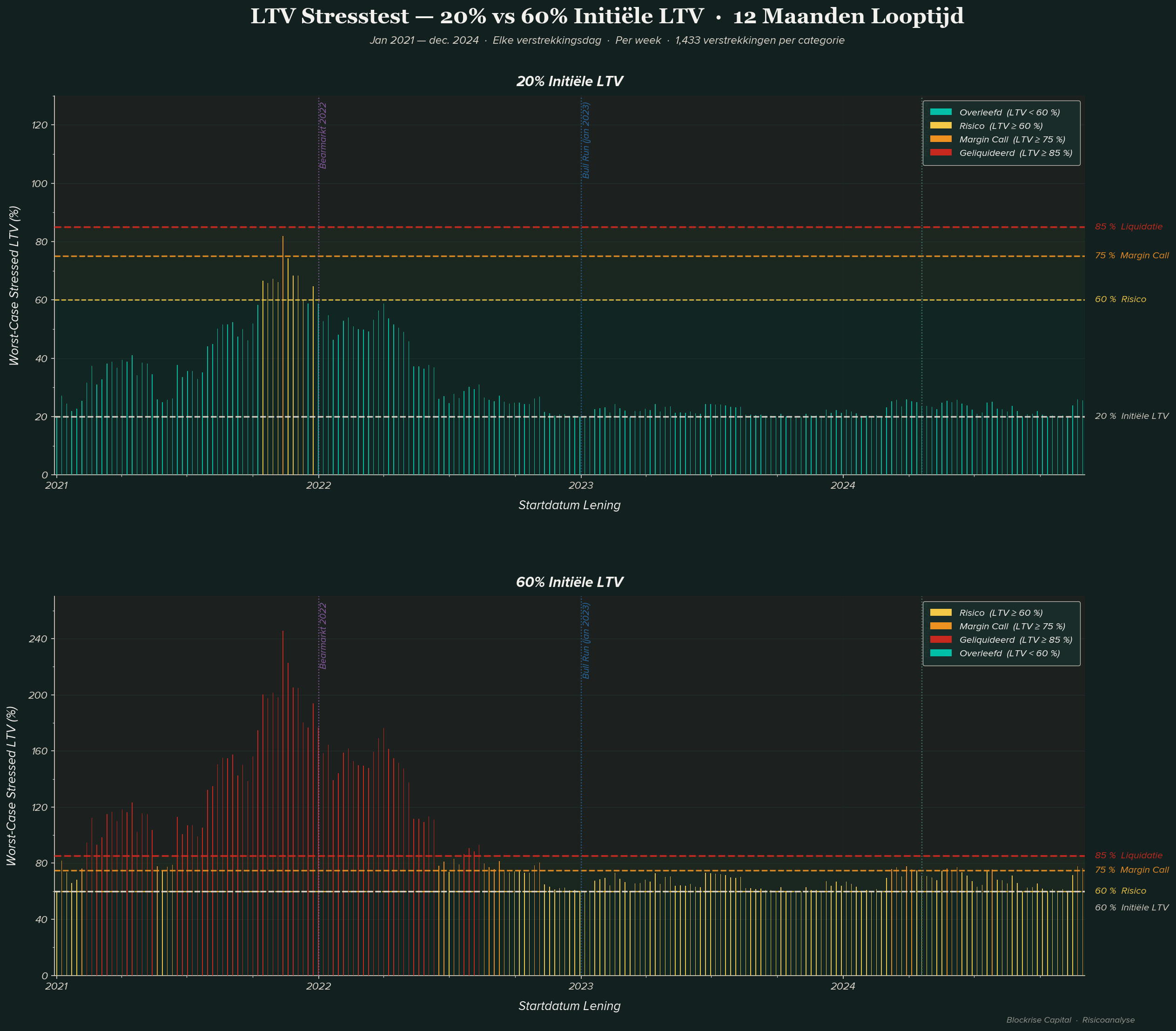

At a 20% origination LTV, only 1.2% of 12-month loans were liquidated, compared to 36.1% at 60% LTV.

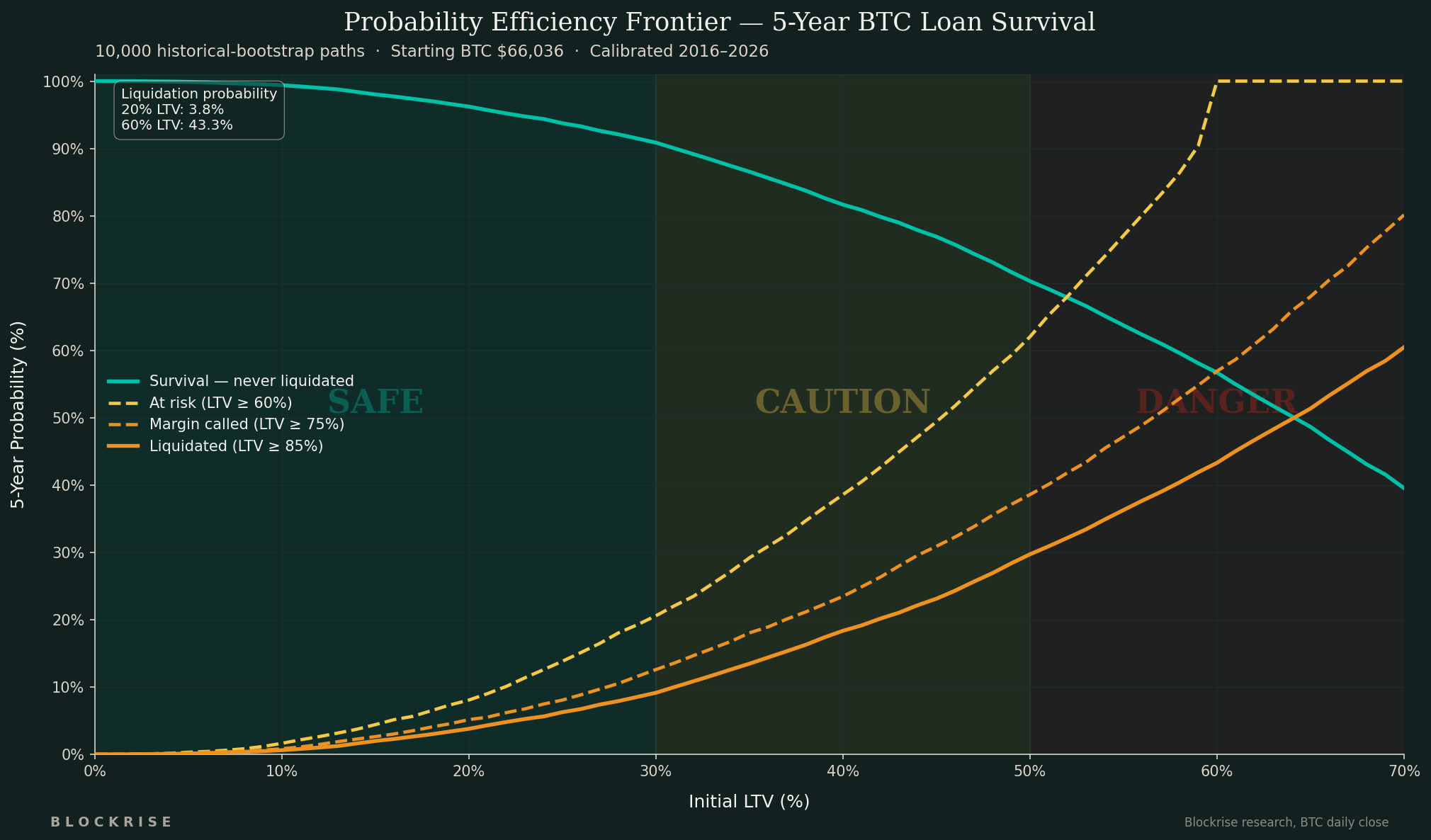

A Monte Carlo simulation of 10,000 Bitcoin price paths shows liquidation probability rising from 3.8% at 20% LTV to 43.3% at 60% LTV.

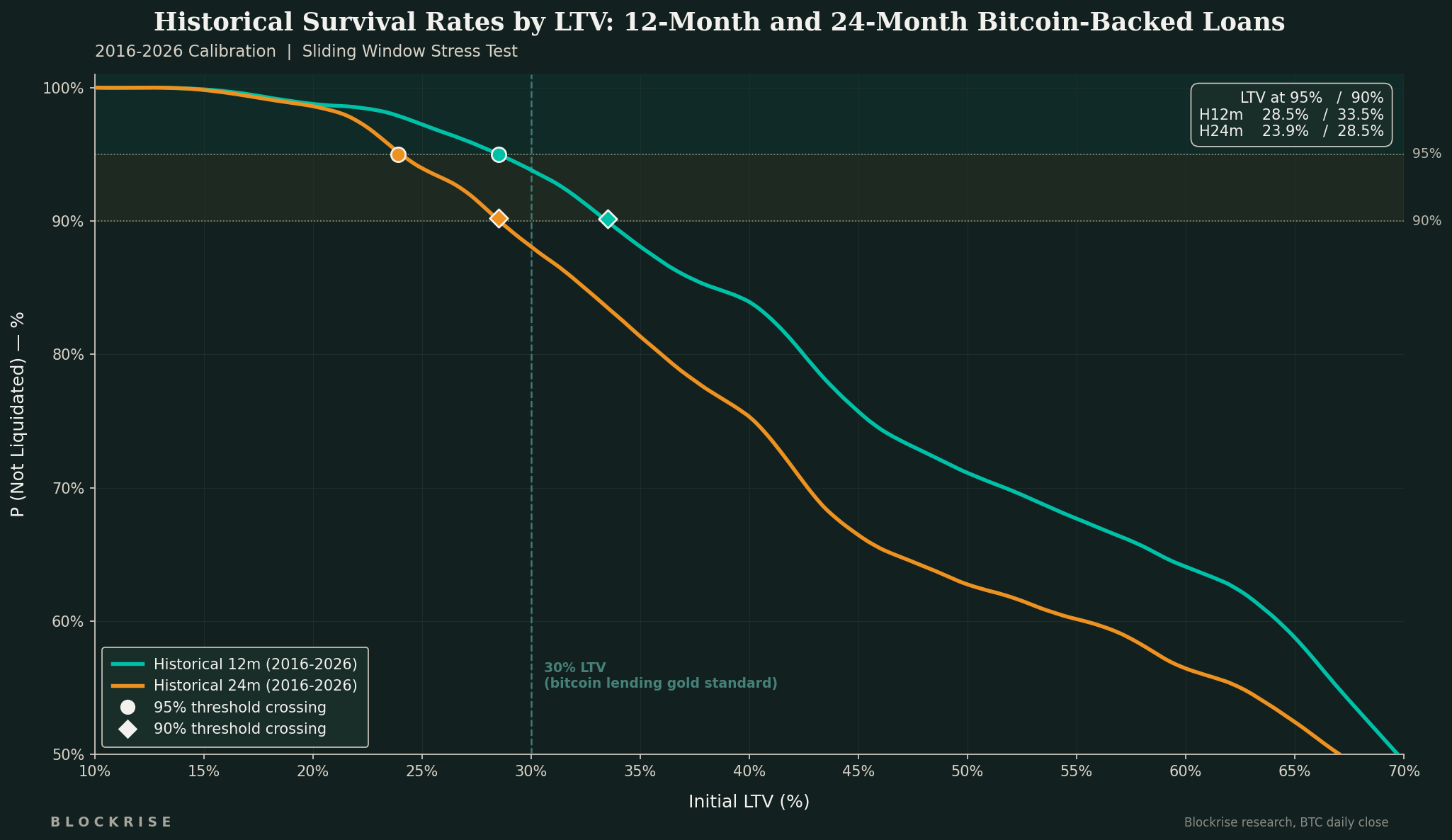

Historical survival curves show that to protect 95% of all past originations, a lender would need to cap initial LTV at 28.5% for 12-month loans and 23.9% for 24-month loans, both below thresholds commonly used in the industry today.

The gap is 34.9 percentage points

The results are stark. At a 20% origination LTV, only 1.2% of 12-month loans across 3,355 originations are liquidated over the entire dataset. At 60% LTV, that figure reaches 36.1% — a difference driven entirely by how much buffer exists when Bitcoin prices fall. The survival of a Bitcoin-backed loan is primarily dependent on one number: the LTV at origination.

What the data makes clear is that the distinction is not that 60% LTV performs badly in crashes, it fails broadly across regimes. The 2018 crypto winter, COVID in March 2020, the Luna collapse, the FTX crash: each event tells a different story about the 60% LTV tier. Meanwhile, 20% LTV only fails in the most extreme events, when Bitcoin drops more than 76.5% from origination within the loan term.

"36.1% of all 12-month loans originated at 60% LTV were liquidated between January 2016 and March 2025, compared to just 1.2% at 20% LTV. The LTV at origination determines nearly everything."

The 2021 cohort sharpens the point. For loans originated at 60% LTV heading into the 2022 bear market, the liquidation rate through that single cycle reached 82.7%, compared to 0% at 20% LTV. The same period, different LTV, entirely different outcomes.ƒ

At 28.5%, 95% of all 12-month loans survived every historical Bitcoin market regime from 2016 to 2026.

How low does the LTV need to be?

Historical survival curves across all regimes from 2016 to 2026 draw a clean line. To protect 95% of all past loan originations, a lender would need to cap initial LTV at 28.5% for 12-month loans and 23.9% for 24-month loans, both below the thresholds commonly used in the industry. The 90% survival threshold eases the requirement to 33.5% and 28.5% respectively.

Notably, the consistent gap between 12-month and 24-month loan survival explains the same phenomenon seen across loan durations: a longer term creates more opportunities for the loan to cross the liquidation threshold. Yet at 20% LTV, the difference between a 12-month and 24-month term adds just 0.21 percentage points of additional liquidation risk — suggesting that at this level of collateral, loan duration becomes almost irrelevant. The dominant variable is the collateral level, not the duration

Risk does not grow in a straight line

A Monte Carlo simulation of 10,000 Bitcoin price paths over a 5-year horizon reinforces and extends the historical findings. At a 20% origination LTV, a loan faces a 3.8% chance of liquidation over five years. At 60% LTV, that figure climbs to 43.3%. The increase is not linear.

Moving from 20% to 30% LTV adds about 5.7 percentage points of liquidation risk over five years. Moving from 50% to 60% LTV adds nearly 14.8 percentage points for the same 10-point increase. The efficiency frontier divides naturally into three zones: a Safe zone below 30%, a Caution zone between 30% and 50%, and a Danger zone above 50%. In the Danger zone, borrowers are penalised disproportionately for every additional percentage point of leverage, while the upper end of the LTV range offers little meaningful protection relative to the risk taken on.

What this means for lenders

The research makes a case that Bitcoin-backed lending is not inherently risky, it is structurally risky when initial LTV levels are set without reference to the full distribution of Bitcoin price behaviour across cycles. A 30% LTV ceiling, currently considered conservative by industry standards, still leaves a lender exposed to meaningful liquidation risk across longer time horizons. The data suggests that a structurally safe threshold sits closer to 25%.

Download the full research paper.

Blockrise™ is a trademark of Blockrise Capital B.V. in the Netherlands and other countries. Blockrise Capital B.V. is a private limited liability company registered in the Netherlands, under Chamber of Commerce number 74879782. Blockrise Capital B.V. holds a MiCAR licence with number 41000029, issued by the Dutch Authority for the Financial Markets (AFM). Blockrise Lending B.V. is a group company and does not hold a MiCAR-license.